Before I sold my house in the Marina district of San Francisco, I always had a slight worry whether it would survive the next big earthquake. The Marina district, although a highly desirable neighborhood in the north end of San Francisco, is mostly liquefaction – a mixture of sand and dirt that was reclaimed from the ocean.

Before I sold my house in the Marina district of San Francisco, I always had a slight worry whether it would survive the next big earthquake. The Marina district, although a highly desirable neighborhood in the north end of San Francisco, is mostly liquefaction – a mixture of sand and dirt that was reclaimed from the ocean.

The last big earthquake was the Loma Prieta earthquake on October 17, 1989 which killed 63 people, collapsed a section of the Bay Bridge, and caused several buildings to burn down in the Marina due to ruptured gas pipelines.

Each time I got the mandatory earthquake insurance offer in the mail, I passed because the deductible (10% – 15% of value of home) was so high and the premium ($5,000+/year) so expensive. I’d ignore the risk I was taking until I’d get the same offer in the mail the next year. I figured worst case, if it burned to the ground, I’d have to spend $650,000 rebuilding a 2,300 sqft structure.

Now that I don’t own a home surrounded by liquefaction, I do feel a sense of relief that I “escaped” almost 13 years of ownership without experiencing a natural disaster. So many people who didn’t live in San Francisco constantly reminded me about the risks of earthquakes before I bought. Then after I bought, so many more people from San Francisco who didn’t/couldn’t buy a home tried to instill fear in me.

What gives folks? Can’t you just be happy for someone’s largest purchase?

As a result of all this feedback, one of my biggest worries was having an earthquake hit while I was in the processing of selling my home. Selling a home is much more stressful than buying a home. If you don’t buy a home, there is no loss except for dashed dreams. If your home falls out of contract when selling, vultures will start circling.

With new devastations seeming to happen around the country every year, I’ve begun to wonder whether it would be wise to look into flood and earthquake insurance again to cover my remaining properties. My homeowner insurance policy cover fire damage, and so should yours.

Natural Disasters Don’t Just Affect Homes

What I didn’t realize was how much damage storms such as Hurricane Harvey can do to cars. It’s estimated that Harvey ruined 500,000 cars by flooding their engines. Similarly, Hurricane Sandy destroyed about 250,000 vehicles and Hurricane Katrina claimed about 200,000 according to Jonathan Smoke, chief economist at Cox Automotive.

Therefore, it behooves everyone to ping their auto insurance companies today and ask what type of coverage they are getting for their premiums. I bet most people have no idea exactly what they are getting for the insurance they are paying. I called my auto insurance company and was reminded I have comprehensive insurance on my new family car with a $500 deductible. I thought I was paying for a $1,000 deductible.

Comprehensive insurance should cover your car from flood damage, hail, a tree falling on your hood, and everything else you can think of. You’ll usually be reimbursed for your ride’s actual cash value (ACV) after you pay your comprehensive deductible.

What’s shocking is that only about 20% of the 1.6 million homes in Harris County, where Houston is located, had flood insurance, according to emailed data from the Insurance Information Institute. For those homes in “high-risk” areas, only 28% of the homes had flood insurance.

Please think about this scenario for a moment. If you have a mortgage to pay, a car to replace, and a home to rebuild out of pocket, there could be no way out of this type of financial disaster except for bankruptcy.

Besides private insurance companies, the federal government offers flood insurance coverage through the National Flood Insurance Program at an average cost of about $700 per year. Of course, the premiums vary depending on your property’s flood risk and value of the house.

For low-risk homes with the maximum coverage of $250,000 for the dwelling and $100,000 for possessions, the premiums are $405 per year, or $452 if you have a basement. For those who have homes of higher value, it looks like private insurance companies are your only option.

Here’s a video that really shows how Hurricane Harvey affected one person’s home and cars. The fella successfully saved three BMWs, but could not protect his home from damage. I’m pretty sure after seeing this video, if you live in a high risk area, you’ll be motivated to call your insurance company!

Deciding On Whether To Get Natural Disaster Insurance

Insurance companies stay in business because they collect more in premiums than they pay out in claims. It’s actually a great business if you look at the profit figures of all the major insurance companies. Therefore, as a consumer, you probably don’t want to get more insurance than is required by law because you know it’ll likely never be used. That said, here’s a checklist that may help you determine whether getting flood or earthquake insurance is a good move.

* Do you live in a high-risk area? If you live in a coastal state, Texas, Louisiana, or Hawaii, you are subject to hurricanes. If you live west of the Rockies, in Alaska, New England, or along the Mississippi River, you are subject to earthquakes. If you live right on the coast, in low lying areas, you are subject to floods. Basically, disaster can strike anywhere at anytime.

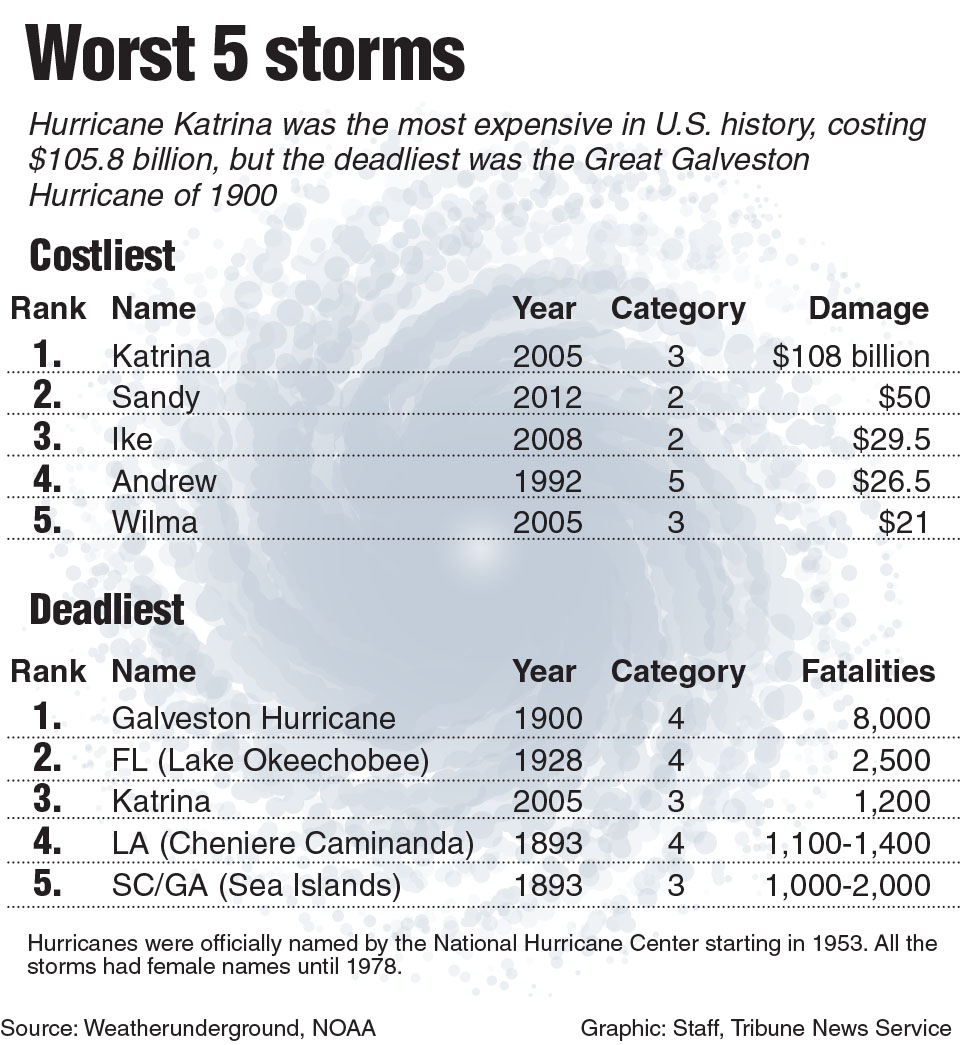

Graphic showing the top 5 costliest and deadliest U.S. hurricanes. [Photo via Newscom]

* When was the last time you invested in disaster mitigation? After the 1989 earthquake, homeowners in danger zones were mandated to “earthquake proof” their homes with stronger foundations. All new construction after 1989 also required stricter foundation construction. As a result, buildings are now safer than ever before. Obviously we won’t know how strong our homes are until angry nature comes, but we should believe the more we invest in disaster mitigation, the better we will come out at the other end.

Although my new primary residence is not on liquefaction, I did spend some money reinforcing the structure and applying new bolts to the frame. Our condo association is spending about $100,000 – $130,000 retrofitting our building by 2018 due to a SF law.

* Have you talked to your long time neighbors? One of the first things I did before and after I bought my house was ask my neighbors how the 1989 Loma Prieta 6.9 earthquake affected our block. One 69 year old neighbor who has owned his building since 1975 told me not a lot happened at all. Some dishes fell off the shelves, but that was about it. However, five blocks west of us several houses had to redo their facades due to cracks. The houses that sustained structural damage were situated 15 blocks away as they were built on top of sand.

Roughly 8 blocks away from my old house in the Marina

* What is the estimate of potential damages? After speaking with my neighbors and doing more research about the 1989 earthquake online, I made a realistic $100,000 damage estimate if a similar 7.0 magnitude earthquake hits. I compared the $100,000 to my earthquake insurance deductible of $150,000 + $5,000 in annual premiums and decided it wasn’t worth it. It’s important each of us assess realistic estimates of what a disaster might cost us out of pocket.

* How big is your emergency savings? The less emergency savings you have, the more you may need insurance. If disaster strikes, you could borrow from your 401K, draw money from a HELOC, or go directly to friends and family.

* How dependent is your retirement on your home? Given our homes are often our largest asset, there’s no doubt many people count on their homes to provide rent-free security once the mortgage is paid off, or rental income if they are a landlord in retirement. Some may even depend on their homes to do a reverse mortgage for income. Whatever the case may be, the higher your home is as a percentage of your net worth, the more you need to consider getting disaster insurance.

* How much equity do you have in your home? This is probably the only situation where having little to no equity is a good thing if disaster strikes. Potential disasters are one of the biggest reasons why people should not pay down their mortgage. If you had the ideal mortgage amount of $1 million, your bank ends up eating the cost if you run away.

If The Natural Disaster Gets Really Bad

The only positive out of a really bad situation is that the Federal Emergency Management Agency (FEMA) might step in to provide grants for emergency repairs and temporary housing. Meanwhile, the Small Business Administration (SBA) may offer up to $200,000 in a low-interest loan for rebuilding.

Rebuilding costs soar during times of emergency, largely due to an upward shift in the demand curve. There will also inevitably be price increases by suppliers of material and services to help mitigate such a surge in demand. Lines for gas at the pump last for hours, while electricity might not come back on for weeks, if not months.

The worst feeling in the world is losing everything and not knowing whether you will ever recover if you don’t have insurance. The second worst feeling during a disaster situation is having insurance, and not knowing whether you will ever collect.

Here’s a video highlighting what type of damage Category 1 – 5 hurricanes can do. Let’s pray Hurricane Irma doesn’t stay a Category 5 when it hits land. For those who are investing in heartland real estate, it’s best to bake in potential natural disaster damages into your returns.

Build Goodwill With Your Insurance Provider

It’s unfortunate to hear so many frustrating stories about insurance companies not paying out a claim when something bad happens. The only thing I can recommend is to go with an insurance carrier that’s been around a long time, has a healthy balance sheet, and use them for multiple financial products to build good will so they decrease the chance of screwing you.

For example, you may want to bundle your auto, property, umbrella policy, and flood insurance together. Your agent will love you, and you will be tiered as a more valuable customer given you’ll be paying higher monthly premiums. As a higher valued customer, they will give you less grief during filing, and will also give you the best rates.

When I filed a $7,500 claim for a lost watch, I spoke to the personal property insurance agent for about 10 minutes, answered seven questions, and got a check for $7,500 three weeks later. They didn’t give me a hard time because they’ve been making lots of money off me for the past 20 years.

More Assets, More To Worry About

With San Francisco temperatures reaching a record breaking 106 degrees, a massive fire spreading in Burbank, California, and Hurricane Harvey slamming Texas, Hurricane Irma on its way, there’s something to be said about having only one car and one house. The ongoing maintenance and insurance costs really start putting a damper on your sense of freedom.

If you’re in an area prone to disaster, at least call up your insurance company and look into the costs and coverage. Compare the insurance premiums to the cost of a total rebuild and make a calculated guess decision. There is no such thing as retroactive insurance.

Each year that goes by without paying insurance premiums is a win. But after many years of winning, you might want to use your winnings to sleep well for the rest of your life.

Related:

How Does An Umbrella Policy Work?

A Preliminary Guide To Auto Insurance

The Ideal Amount Of Homeowners Insurance To Protect Your Family

Readers, do you have flood or earthquake insurance? If so, what is your coverage and monthly premiums? Has your home or car ever gone through a natural disaster? What was the cost to rebuild/replace?

The post Insurance For Natural Disasters: Floods, Fires, Hurricanes, Earthquakes Oh My appeared first on Financial Samurai.

from Financial Samurai https://www.financialsamurai.com/insurance-natural-disasters-floods-fires-hurricanes-earthquakes/

I saw comments from people who already got their loan from Mr Pedro and I decided to apply under their recommendations and just 5 days later I confirmed my loan in my bank account a total amount of $850,000 .00 which I requested for.This is really a great news and I am advising everyone who needs real loan lender to apply through their email : pedroloanss@gmail.com or WhatsApp : +18632310632. I am happy now that I have gotten the loan I requested .

ReplyDelete