Part of the reason why I bought a smaller house in 2014 was because I wasn’t willing to rent my own house for the market price at that time of ~$8,500/month. The price to rent my house had grown from about $5,000/month when I first bought it in 2005. If I had a couple kids and a penchant for throwing tons of money away on rent, then maybe I would have stayed.

Part of the reason why I bought a smaller house in 2014 was because I wasn’t willing to rent my own house for the market price at that time of ~$8,500/month. The price to rent my house had grown from about $5,000/month when I first bought it in 2005. If I had a couple kids and a penchant for throwing tons of money away on rent, then maybe I would have stayed.

To optimize my finances, I figured the best thing to do was to buy a new house more suitable to my house-spending desires (~$5,000/month max) and rent out my old house at market to those willing to pay $8,500/month in rent. This way, economic waste is eliminated, and everybody is happy.

Conduct the same mental exercise with your existing home. If you haven’t rented in a while, you may be surprised by how much your primary residence can command for rent in the open market. The cost of living in your home isn’t the actual money you are spending to live there. The actual cost is the opportunity cost of not renting it out at market rate.

Let me share with you why it’s important to follow the real estate investment rule of Buy Utility, Rent Luxury (BURL) if you want to maximize your lifestyle and your net worth.

Buy Utility, Rent Luxury (BURL)

A common rule a savvy real estate investor follows is to pay no more than 100X the monthly rent as the purchase price. In my example, an investor wouldn’t pay more than $900,000 for my now $9,000 a month rental house.

That said, it’s IMPOSSIBLE to follow this rule when buying in expensive cities such as New York, San Diego, LA, and San Francisco. Even finding properties priced at 150X monthly rent is extremely difficult to find. Why? Because there is excess demand looking to buy property for lifestyle and capital appreciation. Housing becomes more than just basic living expenses, it becomes a luxury option. A Honda Civic takes you around just fine, but some people like to buy classic Ferraris.

I’ve chosen to live and remain in San Francisco because I believe it offers a great combination of wealth creation and lifestyle. The average temperature is in the low 60s, six-figure jobs are a dime a dozen, consulting opportunities are endless, it’s picturesque, the food is amazing, there’s tremendous diversity, and there are plenty of outdoor activities thanks to the topography. San Francisco is amazing, which is why it’s so expensive.

I’d love living in Hawaii, but it lacks a robust domestic economy. With tourism as its main industry, the economy is subject to the whims of others. Unless you are a doctor, lawyer, or entrepreneur in Honolulu, there just aren’t many six-figure jobs. You need to already be rich or have a location independent business to comfortably afford a sweet home.

Rent Luxury Example

Rent this

Although spending $9,000/month ($108,000 a year) on rent sounds expensive, it’s actually good value since you need to spend roughly 303X the monthly rent (25.25X annual rent) to buy my house at market price ~$2.7M. The 100X – 150X monthly rent rule gets blown out of the water.

Even if you owned the $2.7M home outright, you’d still have to pay $33,000 a year in property taxes ($2.7M X 1.2%), $2,500 a year in insurance, and around $5,000 a year in maintenance costs. Meanwhile, your $2.7M could earn a 2.5% annual rate of return risk-free = $68,500 for a total cost of roughly $109,000 if you had no mortgage.

But the reality is that most homebuyers only put down 20%. Let’s say a buyer put down 27% and got a $2M mortgage at a 3.5% interest rate. His annual mortgage interest cost would be $70,000 on top of $33,000 in property taxes, $2,500 in insurance, $5,000 in maintenance = $110,500. Then you must bake in the opportunity cost of not getting a 2.5% risk-free return on the $700K and you get $17,500. The total gross cost of ownership is therefore $110,500 + $17,500 = $127,500 after putting 20% down.

Obviously, renting for “only” $108,000 a year versus owning for $127,500 a year is a financially cheaper option if you don’t include the tax benefits, not to mention the benefits of less maintenance stress. The only way the owner comes out ahead is through principal appreciation and tax deductions. The problem most people have is coming up with the 20% downpayment. Meanwhile, getting approved for a mortgage is much more difficult post financial crisis.

Buy Utility Example

Buy this

Now let’s look at Midwest properties. There are actually $100,000 properties that can earn you $1,000 a month in rent. An $80,000 mortgage at 3.5% after putting down $20,000 only costs the homeowner $359.24/month or $4,310.88 a year. Add on $200 a year in property taxes, $1,000 a year in maintenance, and $500 a year in opportunity cost for not earning a 2.5% risk-free return on the $20,000 downpayment costs only $6,010/year to own compared to $12,000 a year to rent.

If you live in the Midwest, you need to be a buyer of real estate since it’s cheaper and you can cash flow immediately. Capital appreciation is slow compared to coastal city property, but that’s OK because the income generation is so much higher if you begin to accumulate rentals.

So why doesn’t everybody just buy all the Midwest property they can? It’s partly because many people in the past believed that in order to buy Midwest property, you had to live in the Midwest. It’s natural to want to be able to see and manage the property you want to own. Given half the country lives in the coastal cities, half the country focuses on accumulating coastal city real estate. But now, you can surgically buy specific Midwest property through real estate crowdfunding, which is why I’m so bullish on the space. This is financial arbitrage at its finest.

The solution for half the population living in expensive coastal cities such as SF, NYC, LA, San Diego, Boston, Washington D.C. and Honolulu is to therefore rent where you are and buy in the Midwest and South to maximize income and net worth.

What Determines Luxury And Utility?

We can qualitatively say without prejudice that coastal city living can be considered Luxury living while non-coastal city living can be considered Utility living. Who doesn’t want to be near the ocean, see the ocean, fly direct to other countries, eat a wide assortment of food, be constantly entertained, and take advantage of the highest concentration of job opportunities? There’s a reason why expensive cities are expensive.

But of course, non-coastal city people will balk at this classification given there’s so much non-coastal city living has to offer too. There’s something great to be said about a slower pace of living, much lower costs, and lots of space. We’re all biased for where we currently live or where we come from. Therefore, the easiest solution to determining what defines Luxury and Utility is to utilize objective math.

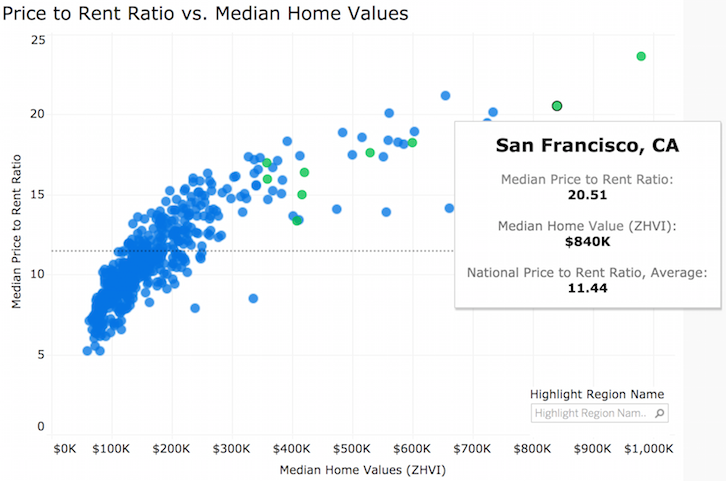

According to data compiled by Zillow, the national Median Price to Rent Ratio is around 11.44 (see dotted horizontal line below). Therefore, we can say the higher a property is valued above 11.44X annual gross rent, the more it is considered Luxury and vice versa.

If we use one standard deviation to determine the Luxury and Utility Median Price to Rent Ratio, the breakpoints are roughly 13.3X and above for Luxury and 9.6X and lower for Utility. In other words, roughly 68% of homes in America trade within 9.6X – 13.3X annual gross rent, which makes renting or owning a wash.

As you can see from the chart, San Francisco (Zillow includes Contra Costa and Alameda counties) trades at a Median Price To Rent Ratio of 20.51X, way above the 13.3X ratio I’ve determined to equal Luxury. However, my rental home trades at 26X annual gross rent, therefore, I should consider selling the property.

Luxury = 13.3X Median Price To Rent Ratio Or Higher

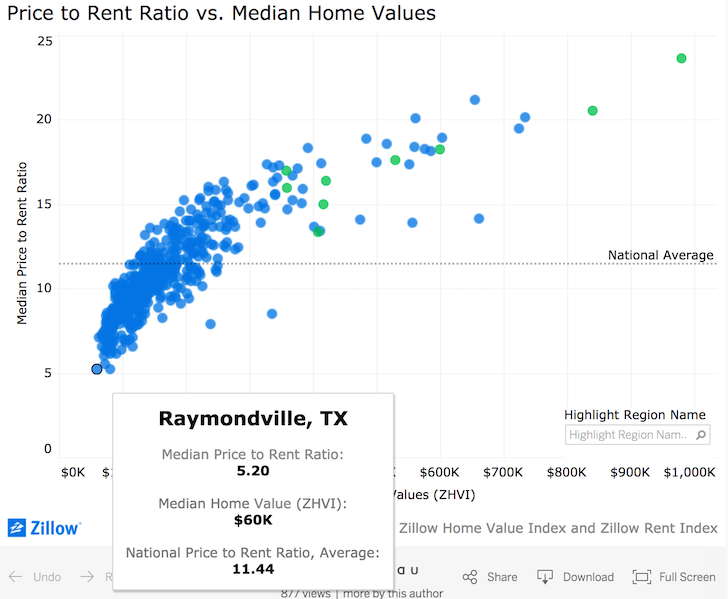

On the flip side, check out properties in Raymondville, Texas with a Median Price to Rent Ratio of only 5.2X. In other words, the median $60,000 house commands almost $1,000/month in rent ($60K / 5.2 = $11,538/year) . In other words, in just 5.2 years, you can have your renter pay back your entire property assuming you took out a 100% mortgage!

Raymondville, Texas clearly is considered Utility, and a savvy real estate investor should be buying Raymondville property all day long if their job market remains stable. The problem is that access to the market hasn’t really opened up yet. Not to worry though, since there are literally hundreds of other towns and cities with properties that trade below the 9.6X Utility classification ratio if you look at the RealtyShares platform.

Utility = 9.6 Median Price To Rent Ratio Or Lower

The Optimal Investment Lifestyle Combo

Of course, real estate is a very personal situation for each individual. We live where we want to live mainly due to our families, friends, and jobs. Not everything is about money. But given this is a blog about ways to optimize our finances, a savvy real estate investor should seriously consider my advice of Renting Luxury, Buying Utility.

Here’s a scenario I’ve been pondering now that I’m in the second half of my life. I want to be closer to my parents and live it up like a boss before I die.

For the sake of dreaming big, there’s this sweet 5 bedroom, 5 bathroom, 6,400 sqft new construction home in Honolulu with a killer view asking $6.95M. Think how many sweet blog posts I can write from the pool! Let’s say the real price is $6.2M since it’s been sitting for a while. Based on a 25X Median Price to Income Ratio, this means I can rent the house for approximately $248,000 a year or $20,500 a month. $20,500 is a lot of money, but think about how much rental income $6.2M can earn in Raymondville, Texas.

First, check out this picture and short video highlighting the $6.2M property. I’m happy to throw a pool party for readers who want to stop by and hang.

Financial Samurai reader pool party anyone?

Seriously, the last thing I want to do is own a humungous house with tons of ongoing maintenance to deal with. But renting it is a different story. Besides, I don’t have $6.2M laying around!

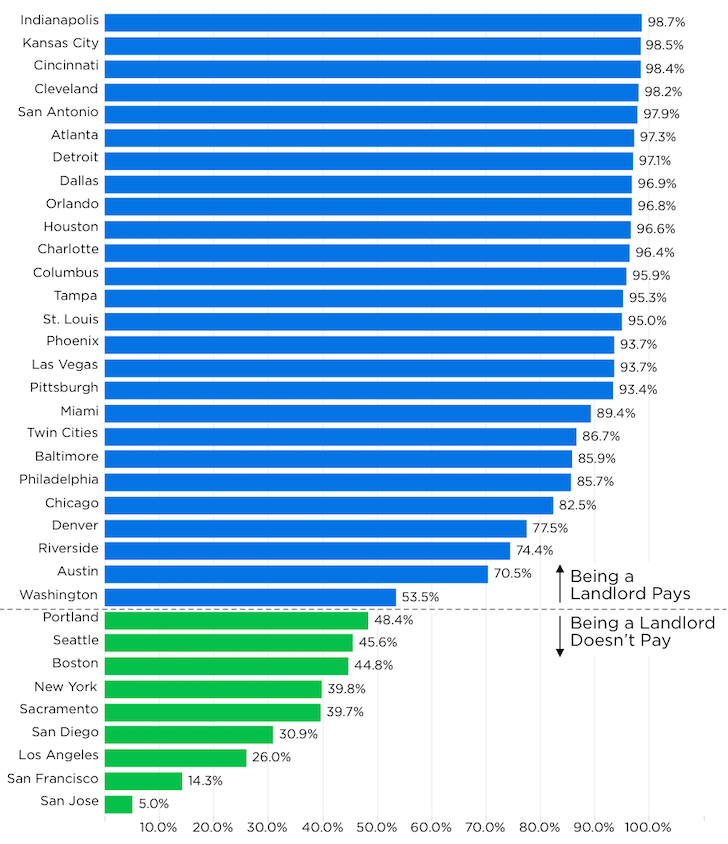

Here’s a shortcut to decide whether it’s better to rent than to buy. The chart shows the share of homes in each city that can be rented out for more than their monthly expenses according to Zillow’s database. Of course, you just can’t buy every single property above the rental profitability line. You must still carefully run the numbers and do your due diligence.

Source: Zillow analysis of Zillow Rent Zestimates and Mortgage Payments, Property Taxes, Insurance and HOA Dues.

The opportunities are plenty to buy cash flow generating properties around the country. Specialized REITs and the rise of real estate crowdfunding companies are making this move easier today. You just need to figure out what type of real estate portfolio mix you want.

For 15 years I’ve been 100% long luxury growth markets. Now I’m shifting towards a balance of growth and income (utility) because valuations are stretched in San Francisco and I don’t have a job.

If you can remove emotion, pride, and prejudice from the equation, you should be able to maximize your lifestyle, cash flow, and net worth. Ready to BURL?

Update 9/27/2017: I sold my rental home in SF for 30X annual gross rent and am reinvesting the proceeds in higher yielding, lower valuation multiple properties across the country.

Related: A Housing Expense Guideline For Financial Independence

Real estate investors, are you following the recommendation of buying utility, renting luxury? What type of growth / income percentage mix do you have in your real estate portfolio? If you live in the Midwest or South, what are some of your reasons for not buying real estate? If you live in a coastal city, what are some of your reasons for buying real estate now after such a massive rise in price?

The post The Real Estate Investing Rule To Follow: Buy Utility, Rent Luxury appeared first on Financial Samurai.

from Financial Samurai https://www.financialsamurai.com/real-estate-investing-rule-rent-luxury-buy-utility/

No comments:

Post a Comment