401k savers rejoice! For 2018, the maximum employee 401k contribution will increase by $500 to $18,500, from $18,000 in 2015, 2016, and 2017. Meanwhile, the employer contribution limit also gets a $500 increase to $36,500, bringing the total annual 401k contribution limit to $55,000 according to an IRS announcement.

401k savers rejoice! For 2018, the maximum employee 401k contribution will increase by $500 to $18,500, from $18,000 in 2015, 2016, and 2017. Meanwhile, the employer contribution limit also gets a $500 increase to $36,500, bringing the total annual 401k contribution limit to $55,000 according to an IRS announcement.

For participants ages 50 and over, the additional “catch-up” contribution limit will stay at $6,000, a level that has stayed the same since 2015. It’s interesting the IRS doesn’t want to give older folks an incentive to save more.

Although your 401k alone will likely be insufficient to meet all your retirement expenses, if you max out your 401k every year, you will likely far surpass the median (~$18,000) and average (~$200,000) household retirement savings held by those between the ages of 56 – 61 today.

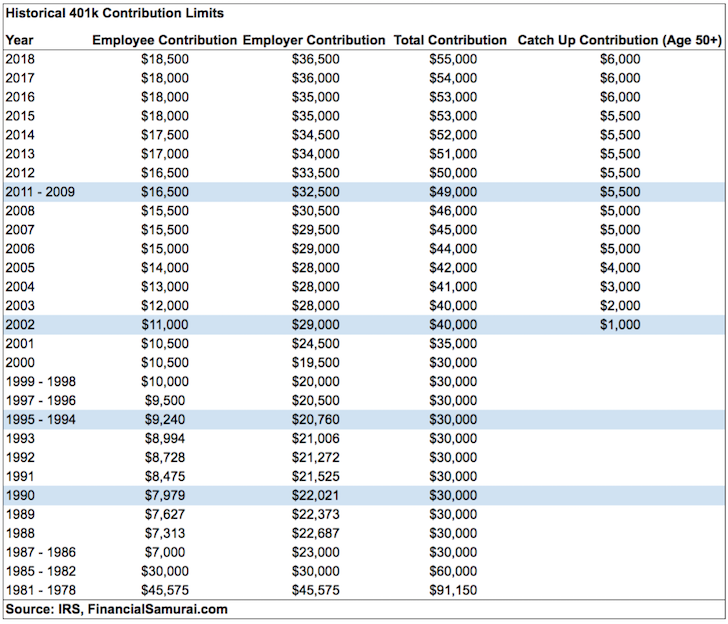

Historical Maximum 401k Contribution Limits (Employee + Employer)

Here’s an updated chart with the historical maximum 401k contribution limits. Notice how much more the employer can contribute to your 401k than the employee. When you hear about employer profit sharing or employer 401k matching, those numbers can now go up to $36,500. It all depends on how profitable and generous your employer is.

For example, those employers who are offering a 100% match up to $5,000 of employee contributions still have $31,500 they can contribute if they truly wanted to. From 2001 to 2012, I worked for a pretty generous employer who during my final five years contributed over $20,000 a year in profit sharing.

For those of you who are now entrepreneurs, freelancers, or work for money-losing startups, not having a 401k or an attractive company contribution is a real opportunity cost. Make sure you calculate these lost benefits before you leave your cushy day job.

For entrepreneurs and freelancers, however, not all is lost when it comes to the 401k because we are allowed to contribute to a Self-Employed 401k (aka Solo 401k) up to the $55,000 maximum if you have enough operating profits. A self-employed person has the right to contribute up to $18,500 to their 401k as the employee, and roughly 20% of the operating profits (revenues minus expenses). Therefore, to contribute the maximum $55,000, the entrepreneur needs to earn at least $182,000 in operating profits.

Here’s a more detailed write-up about how to calculate how much you can contribute to a self-employed 401k plan. Although it’s great an entrepreneur or freelancer can contribute $55,000 in tax-deferred profits to retirement, remember it’s all their money to begin with. Whereas if you´re an employee working for a company, it’s free money.

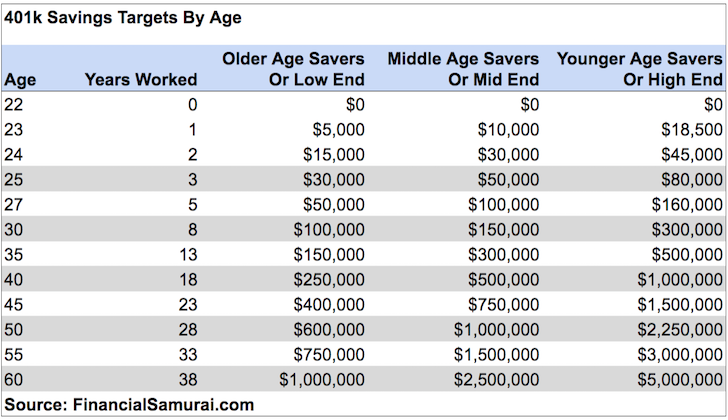

401k Savings Guide By Age

The below is my updated 401k savings guide by age to include various contribution amounts, various contribution limits, company profit sharing amounts, asset allocation levels, and historical stock market and bond market returns. These are all rough estimates to give readers a target to shoot for.

If you are “unfortunate” enough to only work until age 35 at a company with a 401k plan, then you can shoot for a 401k savings range of between $150,000 – $500,000. If you are fortunate enough to work for 38 consecutive years at a company with a 401k plan until you’re allowed to withdraw penalty-free, then your target savings is $750,000 – $5,000,000.

As a Middle Age Saver (40 years old), I started my 401k contribution in 2000 when the contribution limit was just $10,500. Therefore, I’m more focused on the Mid End column to get to $2,500,000 by the time I turn 60. Even if I contribute $35,000 a year for the next 20 years to my Self-Employed 401k plan, I’ll need the stock market and bond market to rise by at least 3% a year to get to $2,500,000. In other words, when it comes to investing, there are no guarantees. You must take a certain level of risk.

The “Younger Age Savers Or High End” column is the 401k savings potential for those just out of school and who have generous employers. In every scenario, an individual who contributes for 38 years will become a millionaire. Unfortunately or fortunately, not everybody will work for such a period of time.

Motivation For Maxing Out Your 401k

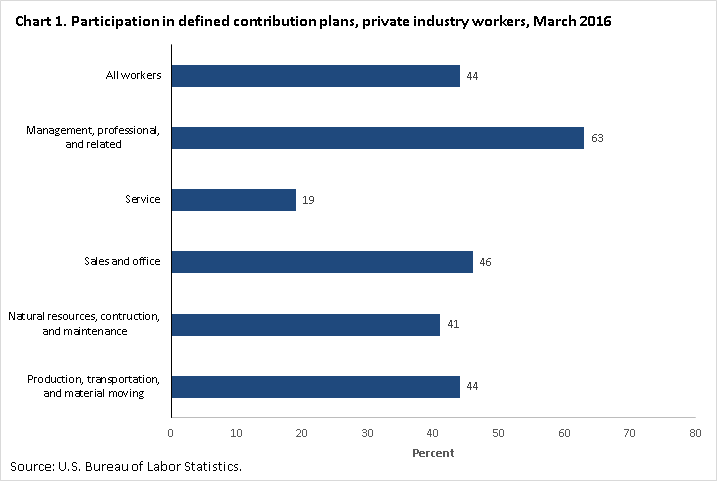

I really hope everybody who has a job that provides a 401k plan takes full advantage. To not do so is completely foolish. Below is data from the Bureau Of Labor Statistics regarding the latest participation rate in defined contribution plans like the 401k.

A 44% participation rate is not bad, but the number should be 100% if you are a Financial Samurai reader. Further, you can bet that only a minority of the 44% max out what they can contribute to their pre-tax retirement savings plan, otherwise, how else would you explain only a ~$18,000 median and $200,000 mean average retirement savings amount for 56 – 61 year olds. My hope is for 100/100, meaning every reader hear maxes out their plans for as long as you are able.

Here are some thoughts to get you motivated to max out your 401k.

1) Remind yourself a 401k is only one leg of the retirement stool that is already broken. The other two legs of the retirement stool are a pension and Social Security. According to the Bureau of Labor Statistics about 22% of full-time private industry workers have a defined pension benefit compared to 42% in 1990. Although most public sector employees still get pensions, public sector employees account for only around 10% of the population. In other words, most people don’t have pensions anymore.

As for Social Security, the realistic calculation is that when eligible, we will still all receive Social Security checks, but at 70% of what is currently promised if nothing is changed. Given most people don’t have pensions and Social Security won’t be paid in full, the 401k is an integral part of your retirement plan.

2) Calculate a budget based on a $18,500 reduced gross income. Nobody really sits down and writes out their expenses. We’re either afraid or lazy for some reason, yet we can spend hours doing research on our next big screen TV or laptop. But for your own sake, take your current income, subtract $18,500, and multiply it by one minus your effective tax rate to calculate your disposable income e.g. $100,000 – $18,500 = $81,500 X (1-25%) = $61,125 after taxes and 401k max. Divide the annual income by 12 to get a monthly disposable income figure and work your budget from there. The bigger the buffer you can have from spending all your disposable income, the better.

3) Make your contributions automatic. As soon as you make your maximum contributions automatic, you will adapt your lifestyle to your paycheck. Automatic contributions will save yourself from yourself. It’s exactly like the government withholding federal income taxes each paycheck because they know you won’t pay your full tax liability at year end. Making your contributions automatic will make savings so much easier. You will wake up 10 years from now and be amazed at how much you have accumulated.

4) Envision your 60 year old self working the cash register at McDonald’s. One of my biggest motivators for saving and paying down debt was seeing senior citizens working minimum wage jobs. While I admired them dearly for continuing to work, they also scared me straight into saving more because I didn’t want to be them one day. Instead, I wanted to be relaxing on a beach with a Mai Tai in one hand watching the sunset with my lovely wife. The more we can envision ourselves in poverty, the more incentivized we can be to max out our 401k.

5) Do it for your family. If you’re not willing to get in shape, save aggressively, and invest wisely for yourself, then at least do so for your family. There’s not a day that goes by where I don’t think about ways in which to give my son and my wife a better life. When you know you’ll likely die before your spouse and child, you’ll start focusing on your finances much more seriously.

Note: There is a poll embedded within this post, please visit the site to participate in this post's poll.Diversify Your Retirement Savings

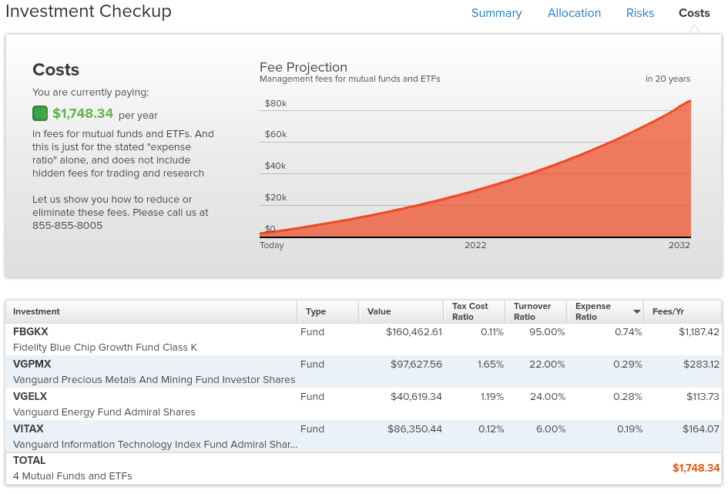

Once you start contributing like a champ to your 401k, run your 401k through a 401k fee analyzer to see how much in fees you are paying. I discovered I was paying a whopping $1,748 in annual 401k fees when I thought I was paying maybe $200 a year. Over a 20 year period, my fees would climb to ~$90,000, provided my portfolio also increased as well.

For those who seek to retire before 60, it’s important to also to save and invest as much as possible in your after-tax investing account. Ideally, your goal should be to grow your after-tax investment account larger than your 401k by the time you’re ready to retire. Make your after-tax investment contributions automatic with each paycheck as well.

The chance of you working for 38 years at a company with a 401k is not high. Therefore, you shouldn’t rely on your 401k for retirement. Instead, look at your 401k as a bonus you’ll get to use once you pass the age of 60. I plan to have over $2,500,000 in bonus money in 20 years. How about you?

Regards,

Sam

The post The 401k Maximum Contribution Limit Finally Increases For 2018 appeared first on Financial Samurai.

from Financial Samurai https://www.financialsamurai.com/401k-maximum-contribution-limit/

No comments:

Post a Comment