Reflection helps us appreciate how far we’ve come. Reflection also helps us learn from our mistakes. In this post, I’d like everybody to reflect on several key items: Career, Finances, Health, Family, and Happiness. See if you can tie the five together and weave a story about who you are today.

Reflection helps us appreciate how far we’ve come. Reflection also helps us learn from our mistakes. In this post, I’d like everybody to reflect on several key items: Career, Finances, Health, Family, and Happiness. See if you can tie the five together and weave a story about who you are today.

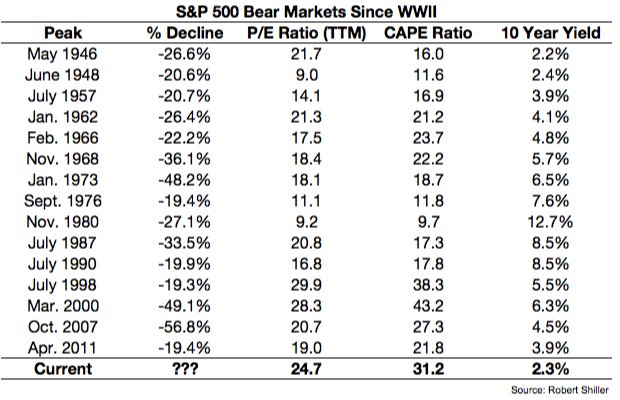

The one thing I know for sure is that 2017 feels a lot like it did 10 years ago. But this time, every asset class is expensive. I’ve got folks asking me about investing in cryptocurrencies when they haven’t even invested in stocks. Other folks are asking whether they should use their HELOC to buy another property with an 80% loan-to-value ratio. Everybody has maximum investing FOMO right now!

It’s an exhilarating time, but it’s also a perilous time for those who don’t have perspective.

Life In 2007

Career: I was finishing up my third year as a VP at a large investment bank in San Francisco. 2007 was also the year I turned 30. Given my boss recently departed to become a client, I was left to take over the west coast business. Knowing my worth, I asked for a raise and a promotion and got them. If they lost me to a competitor, they would have been screwed for at least six months as they scrambled to find and train my replacement.

30 years old was a significant age because I finally felt like I could be taken seriously. Getting my MBA in 2006 also gave me a confidence boost. I was loving my career because I was finally my own boss in San Francisco. Sure, I had to work with the head of the office and a more senior colleague in a different department, but for the most part, I was free to control my own schedule. So long as the business was coming in, nobody could complain.

In 2007, I thought I could easily work for 10 more years and then call it quits for good. Little did I know the financial crisis would crush my industry and cause me to pursue a different path just four years later.

Related: A List Of Career Limiting Moves To Blow Up Your Future

Finances: I received the biggest bonus of my life in 2007 due to a negotiation I had with my big boss in Hong Kong. It was a handshake agreement, so you never know until the end of the year when bonuses are paid. But he delivered as promised. From that day on, I decided to be loyal until the very end.

Although the stock market was booming, I was still hesitant to go all-in due to the dotcom bubble that began to collapse in 2000. Instead of investing everything I had in the stock market, I decided to invest most of my savings in real estate. At least with real estate, if all went to hell, I’d still have something to sleep in.

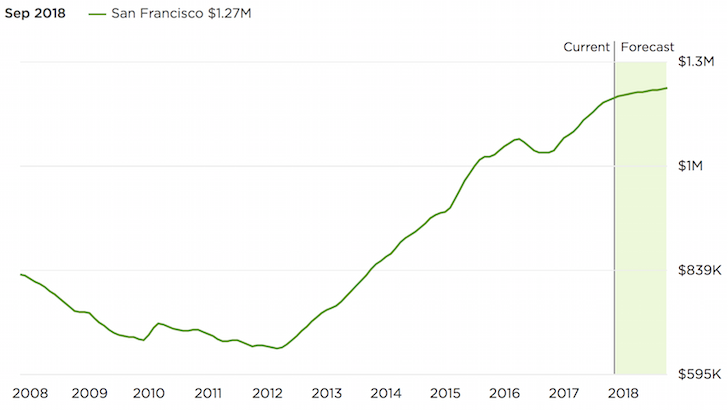

I bought my first SF property in 2003, lived in it for two years, and was renting it out to a couple in 2007. In 2005, I decided to take out a $1,200,000 mortgage and buy a single family house in the Marina district for $1,523,000. It was the cheapest house for its size in the neighborhood because it was on a busy block next to the busiest street.

Because my real estate investing experience was positive, and I had just received a big bonus, I decided to buy a $718,000, 2/2 vacation condo at The Resort At Squaw Creek, Lake Tahoe in 2007. I loved the place because that’s where I took my girlfriend on our first getaway date back in 2001.

I was delirious about my financial luck and felt I just couldn’t lose. I was imagining that my compensation would continue to grow by 10-20% a year for the next five years. There were some warning signs about the stock market and real estate market getting ahead of themselves, but I didn’t listen carefully. Instead, I myopically focused on my fortunate career situation. I wish someone with decades of experience sat down with me to run through the pros and cons of buying more property then.

Notice the frequency. Nobody know when the next downturn will begin.

Health: Work was stressful given the 60-70 hour work weeks. But at least my chronic back pain from 2000-2003 was gone. But what replaced my chronic back pain was teeth grinding and TMJ. It hurt to speak for more than an hour. I remember paying $700 to a specialist dentist who ground down parts of my molars so I could get some relief when I closed my jaw.

I was in OK shape because I started aggressively playing tennis again. But of course, I suffered from occassional tennis elbow pain that kept me from swinging freely. I weighed between 162-165 lbs, which was a normal weight for someone 5’10” tall.

Now when I look back on my diet, I realize I ate extremely unhealthy due to frequent client entertainment. I’d often take clients to fancy steak restaurants and nice lounges. The wagyu beef and Moscow Mules tasted especially good thanks to a corporate card with a $200/head budget.

I remember telling myself that no matter what, living in San Francisco was healthier than living in Manhattan.

Family: My girlfriend graduated college in 3.5 years and came out to live with me in December 2001. She was 27 in 2007, and I was unsure whether starting a family was a good idea yet. Work was extremely busy and I had all this pressure to keep the ship afloat given my boss left.

But I knew she was the one, so I proposed during the heart of the financial crisis in 2008. We got married in Hawaii in December 2008.

If the financial crisis didn’t hit, I would have been more confident to start a family by 2010. It would have been nice to get parental leave and company benefits. Further, since our son is the best thing that has ever happened to us, he would have been in our lives for seven years longer.

It’s so difficult to figure out when is the best time to have children. Even if you decide now is the time, it might take several years to conceive.

What I do know is that having a life partner through my entire post college journey has been priceless.

Related: When Is the Best Time To Have Children? A Physical And Financial Decision

Happiness: I was ecstatic about getting a raise and a promotion. Part of my happiness stemmed from having gone to public high school and public university. Never in my wildest dreams had I thought I’d have a job at a respectable investment bank and earn a healthy income. If I had gone to an elite private school, I’m not sure I’d be as happy because I would have expected all these things and more.

It’s funny, but the memories that stands out most from this time period were figuring out what ring to buy and the cozy little wedding on our favorite beach in Hawaii the next year.

My happiness level has never really fluctuated much since graduating from college in 1999. It’s always been about a 7-8 out of 10. The happiness of getting recognized at work only lasted for maybe three months. The pressure to deliver took over.

Life in 2017 And Beyond

The most important thing I learned from 10 years ago is thinking that I couldn’t lose, and then losing big when the financial crisis hit in 2008. I remember swearing to myself in 2010 that if my investments ever came back to pre-crisis levels I would take some money off the table. I tried to do so in 2012 by selling my primary residence in order to pay off a ~$1,000,000 mortgage and live in a small two bedroom, one bathroom apartment. But nobody wanted to buy my four bedroom house.

The difference with 30 year olds in 2017 versus my 30 year old self in 2007 is that I went through the dotcom collapse in 2000. I saw paper millionaires end up with nothing within a couple years. They had to start all over, like the guy who made my breakfast croissant each morning. As a result, I tried to diversify as much as possible.

It’s hard to really know how scary recessions can be if you’ve never been in one with significant money at stake. Everybody likes to say they’ll hold on to their investments and buy more during a downturn. But when your investments are down 30%+ and many of your colleagues are getting fired, the first thing you do is think about survival, not dumping every last cent you have in the stock market.

I’m praying that I’ll finally be satisfied with what I have today and no longer grind as hard. My health depends on it. Staying in San Francisco and being surrounded by so many success stories has finally taken its toll. My recent bout of chronic back pain reminded me not to forget the point of financial independence and owning a lifestyle business: a better life.

Some Final Thoughts

* It’s easy to extrapolate explosive growth in your career and net worth in a bull market. The problem is, nobody wants to work forever and things always change. Be more conservative with your expectations. Don’t confuse brains with a bull market.

* No matter how much money you make or have, your steady state of happiness won’t really change. Stop thinking that if you get to X amount you will be happy. Retire by a certain age, not a financial figure. There will always be something that will give make you feel bad. But the good thing is, you’ll likely revert back to your steady state.

* If you’re relatively young (under 40), it’s worth swinging for the fences during the good times. It’s worth allocating some funny money to chase unicorns. Money is abundant and cheap. Once the spigot shuts off, dumb ideas no longer get funded and silly job offers are no longer given.

* Learn when to cash in your chips by setting goals. You made these goals because you decided how much was enough. If you’ve somehow found yourself way beyond your goals, then absolutely focus on using your profits for a better life. The saddest thing is losing a massive lead.

* Even if you buy at an inopportune time, if you wait long enough, you’ll likely eventually get back to even. Just look at us now.

* The next 10 years will go by faster than the previous 10 years. Make the most of it.

Related: Recommended Net Worth Allocation By Age Or Work Experience

I’d love to hear about where you were 10 years ago, and what you learned about yourself then that you will apply to your life now? Time truly accelerates the older we get. Let us not waste a single minute.

The post It Feels A Lot Like 2007 Again: Reflecting On The Previous Peak appeared first on Financial Samurai.

from Financial Samurai https://www.financialsamurai.com/feels-lot-like-2007-again/

No comments:

Post a Comment