There’s a ton of talk about how there’s a housing affordability crisis in various parts of the country.

There’s a ton of talk about how there’s a housing affordability crisis in various parts of the country.

Perhaps the fear of forever being priced out is an underestimated motivating force behind the continued demand for housing despite high prices.

I remember when I bought my first 2/2 condo in 2003, I felt a sense of relief that I no longer had to pay ever-rising rents. Even though the $2,300/month mortgage payment was about 15% higher than my previous rent after a 25% down payment, it felt good knowing my costs were generally fixed.

What I’ve recently realized is that many people in San Francisco and many other cities have not had to pay a single penny for housing costs over the years.

What? How is this possible when San Francisco is considered one of the most expensive cities in America?

Let me show you with a friend’s example that doesn’t involve mooching off your parents as an adult child.

How To Live For Free In An Expensive City

Here’s the profile of a home that was purchased for $1.3 million in 2011 and sold for $2.2 million in early 2019. He put down 20% and took out a $1,040,000 mortgage at 3.5%. Below are some approximate numbers.

Positives

- Monthly rent avoided for eight years: $5,500

- Total rent avoided after eight years: $440,000

- Net proceeds after fees, principal pay down, all taxes from selling house: $1,100,000

Negatives

- Opportunity cost of not investing $260,000 (down payment) in the stock market from 2011 – 2019 = $286,000 (110% appreciation)

- Net mortgage interest cost after eight years = $203,000

- Net property taxes after eight years = $90,000

- Maintenance cost after eight years = $20,000

Net cost of living = ($440,000 + $1,100,000) – ($286,000 – $203,000 – $90,000 – $20,000) = $941,000.

If this simple math is right, not only was my friend’s family housing free for eight years but he was also paid $941,000 to live in San Francisco. That’s pretty good value for just living.

Obviously, experiencing a 69% appreciation in his property was a big factor in this equation, but so was not having to pay $440,000 in rent during this time period.

Even if the property only appreciated by 3% a year, my friend would still have been paid over $500,000 to live in San Francisco for eight years.

Related: Reinvestment Ideas After Selling A House

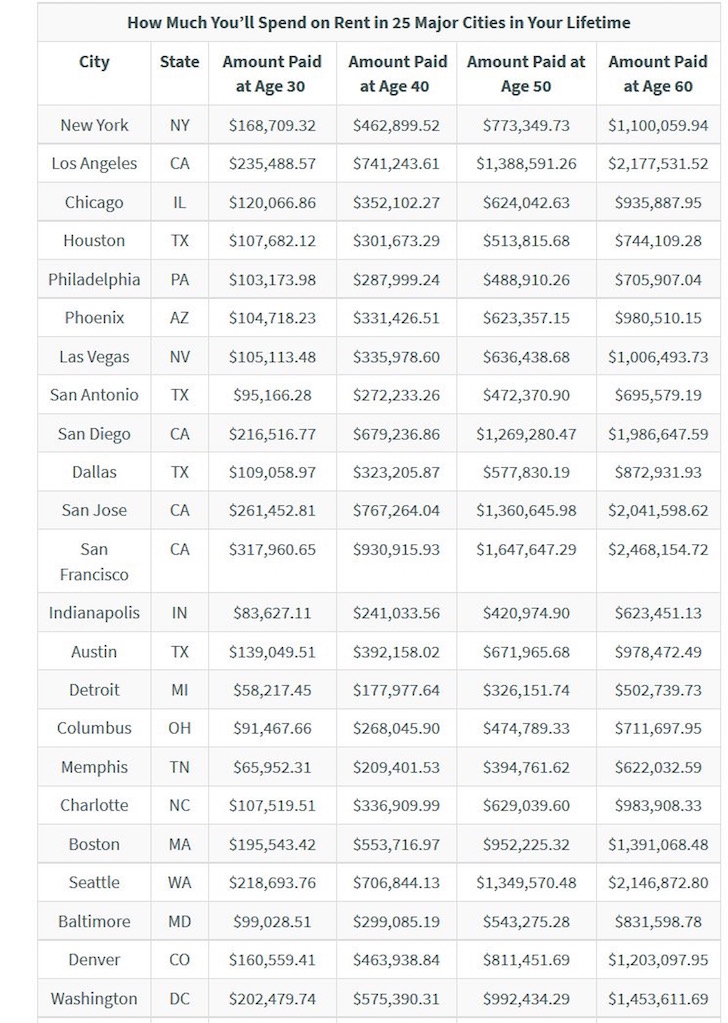

How Much You’ll Spend On Rent In Your Lifetime

Check out this chart about how much money you’ll spend on rent for a median-priced home in various major cities.

It’s kind of crazy to see that a San Francisco resident would pay $2,468,000 in rent for a median-priced property by the time he or she turns 60.

Is your city on the list? If not, add up how much you’ll end up spending on rent for your desired property if you never buy. I don’t think you’ll like the results.

With such massive amounts paid in rent over one’s lifetime, is it no wonder why the desire to buy property is so strong?

I’d love for property prices to decline by 20% so I can snap up another Golden Gate Heights panoramic view property in San Francisco. Alas, unless I get really lucky, another investment property is not in my cards.

Some Takeaways On Getting Paid To Live

1) The return on rent is always -100%. Yes, you get a place to live, but if you buy, you also get a place to live. Once this variable is canceled out, what’s left is the owner’s optionality to sell the asset. Who said high school algebra was a useless course.

2) Although buying a home is making a concentrated bet with leverage, buying a home may ironically be easier than investing the same amount of money in the stock market because you’re buying a tangible asset that may improve the quality of your life. With stocks, there is not utility gained. Further, prices could decline out of the blue.

3) Renting and investing the difference in the stock market and other assets is a great idea, but people often fail due to a lack of financial discipline. Without a proper automatic invest strategy in place, chances are high the saved difference ends up getting spent or left sitting in a bank account.

4) Time is your friend when it comes to owning a property. Over time, the cost to rent rises to barf-inducing levels. Meanwhile, the appreciation of a property also sometimes rises to unbelievable levels. The only way you can survive as a renter is if rents stay flat or go down, which usually doesn’t happen due to inflation. Rising rents and rising property prices will crush your financial progress if you are unwilling to get neutral real estate by owning your primary residence or moving to a lower cost area.

5) To live for free, you’ve got to take risk. Staying in a rent-controlled apartment is somewhat akin to working at a safe day job with no upward mobility. You’ll likely never starve, but you’ll likely never get rich either. If you take some risk by buying real estate, you might do very well just like if you decided to start your own business or hop to a different employer. Alternatively, you might go bankrupt if you buy inappropriately. But at the end of the day, no risk no reward.

6) Living for free strengthens the real estate market further. Living for free is another phrase for rising home equity. The more home equity there is, the larger the buffer in case of a recession. Given lenders have significantly tightened their lending standards since the 2009 financial crisis, only the most credit worthy borrowers have bought homes.

When you combine high credit worthiness with record high home equity and low mortgage rates, it’s hard to see another crash in home prices again. The best we can hope for is a 10% – 15% decline window before another recovery. Instead, we’re likely going to see increased discretionary spending.

Arbitraging To Live For Free

Once you own your primary residence, you won’t truly know until after you’ve sold your property whether you lived for free all those years or not. In the meantime, you can make educated estimates every year about whether buying or renting made more sense.

If you really want to live for free in the present, you’ve got to figure out a way to make investments that will produce income that will cover all your housing expenses and then some.

The concept of Buy Utility, Rent Luxury (BURL) is one logical strategy. Aggressively saving money on the short end of an inverted yield curve to cover your longer duration borrowing costs is another strategy, especially when the yield curve is inverted.

But the easiest strategy is to simply not rent for life. If you rent for life, you are going to look back 30 years from now with regret. Your kids will also likely hate you for not buying so long ago.

All these rich kids today are rich because their parents had the foresight to do some math and take some calculated risk decades ago.

If you’re not willing to build assets for yourself, at least do it for your children. Just make sure the numbers make sense.

Related: Focus On Trends: Why I’m Investing In The Heartland Of America

Readers, have you been living for free all these years? If so, I’d love to hear about your numbers. Despite all the data that shows homeowners are on average 44X richer than renters, why are there still so many people against long-term homeownership to build wealth?

The post The Return On Rent Is Always Negative 100 Percent: Here’s How To Live For Free appeared first on Financial Samurai.

from Financial Samurai https://www.financialsamurai.com/return-on-rent-is-always-negative-100-percent-how-to-live-forfree/

No comments:

Post a Comment